The Characteristics of Individual Income Tax in Singapore

Tony

Tony

August 24, 2020

August 24, 2020

As a country open and connecting to the world, the tax policy in Singapore is relatively more friendly than many other countries, so it can attract more international investment and professionals. But how friendly it is? I will elaborate starting from the individual income tax policy in Singapore.

Taxpayer

Defining taxpayer is to define who need to pay individual income tax.

All Singapore Citizens and Singapore Permanent Residents are tax residents in Singapore. As a foreigner, if you stay or work in Singapore for at least 183 days in a calendar year, you are also a tax resident in Singapore. Tax residents in Singapore are taxed at progress resident rates.

As a foreigner, if you stay or work in Singapore for 61 to 182 days in a calendar year, you are taxed at non-resident rates.

As a foreigner, if you stay or work in Singapore for no more than 60 days, you do not need to pay individual income tax.

The definition of individual income taxpayer in Singapore is quite common compared with most countries. Its friendly part is that Singapore only tax income generated locally. It does not tax any income received from overseas.

Taxable Income

In Singapore, taxable income includes employment income, self-employed income, rental income from properties. On the other hand, the following items may be taxed in other countries, but they are not taxable in Singapore: interest received from deposits, dividend distributed by local listed companies, gain from selling local listed company shares, and windfalls (winnings from legal betting).

Tax Relief

There are many items eligible for tax reliefs or rebates in Singapore. They represent the social direction advocated by the government. Common tax relief items include: CPF (contributed by employee, contributed by employer and voluntary contribution), self-employed expenses, property rental expenses, donations, life insurance premium, SRS, earned income relief, course fees, supporting family members (such as parents, grandparents, siblings, spouse and children), NSman relief, foreign maid levy (in order for local female taking up employment), working mother relief, etc. I elaborated this part in my previous articles Guidelines on Tax Relief Items in Tax Filing and Tax Relief Benefits for Working Mothers in Singapore.

Tax Rate

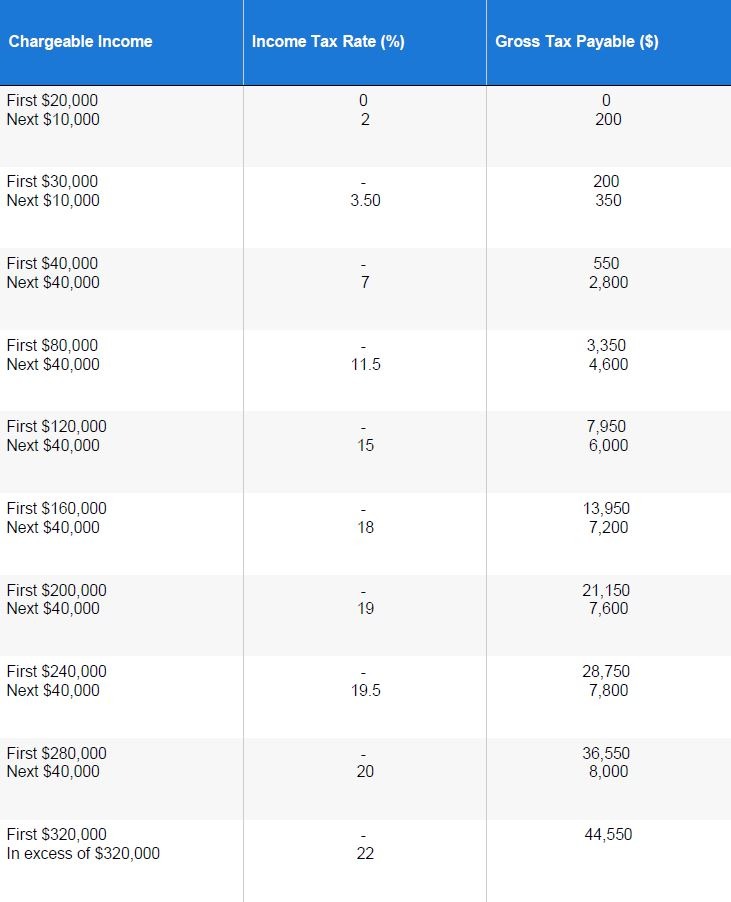

Tax residents in Singapore are taxed at progress resident rates. Annual income no more than $20,000 is not taxable. The part of annual income exceeding $20,000 is taxed from 2% to 22% based on different tiers. The specific tiers are illustrated as follows:

Source: Inland Revenue Authority of Singapore (IRAS)

Here we do calculation for one example. Assuming Mr Zhang is working in Singapore. His annual income after deducting all the relief items is $60,000. His income tax is ($60,000 – $40,000) × 7% + $550 = $1,950.

Let’s make a comparison with China, simply using the exchange rate of 1 SGD = 5 CNY. If Mr Zhang is working in China, and his annual income after deducting all the relief items is CNY 300,000, his income tax will be CNY 43,080, equivalent to SGD 8,616.

From this comparison we can tell that the individual income tax rate in Singapore is generally lower than that in China.

This article is just at introductory level about the tax policy in Singapore. If you have any relevant questions, welcome contacting me for a discussion. I will also address your popular questions in my future articles.